Exploring the World of High-Yield Savings Accounts and Their Benefits

advertisement

In an era of economic uncertainty and rising inflation, making your money work harder is no longer optional—it’s essential. It be possible to keep a good in traditional savings accounts. place to stash cash, their near-zero interest rates often leave savers feeling shortchanged. Enter high-yield savings accounts (HYSAs), the modern solution for growing your savings with minimal risk. This guide dives into the mechanics, advantages, and strategic uses of HYSAs, empowering you to maximize your financial potential.

1. What Exactly Are High-Yield Savings Accounts?

recoverer who want A high-yield account should look at it. Unlike traditional accounts, which may offer 0.01% APY (Annual Percentage Yield), HYSAs often boast rates 10–20 times higher, currently ranging from 4.00% to 5.50% APY as of mid-2024. It's possible to offer these accounts online. banks or fintech companies, which pass on savings from lower overhead costs to customers.

Key Features:

- FDIC/NCUA Insured: Funds are protected up to $250,000 per depositor.

It exist leisurely to access money without being Liquidity. Federal regulating limit the amount of penalties. withdrawals to six per month).

there isn't any necessity for a minimal balance requirements. Start with $1 and you'll be able to see how much you comparable it.

2. HYSA vs. Traditional Savings: Why the Difference Matters

The primary advantage of HYSAs is their ability to combat inflation. With the U.S. inflation rate hovering around 3.5% in 2024, a traditional savings account earning 0.01% APY effectively loses purchasing power over time. In contrast, a HYSA earning 5.00% APY not only preserves your money but grows it in real terms.

Example:

- $10,000 in a HYSA at 5.00% APY = $10,500 after one year.

- The same amount in a traditional account at 0.01% APY = $10,001.

This stark difference underscores why HYSAs are critical for anyone prioritizing financial growth without exposure to market volatility.

3. The Top Benefits of High-Yield Savings Accounts

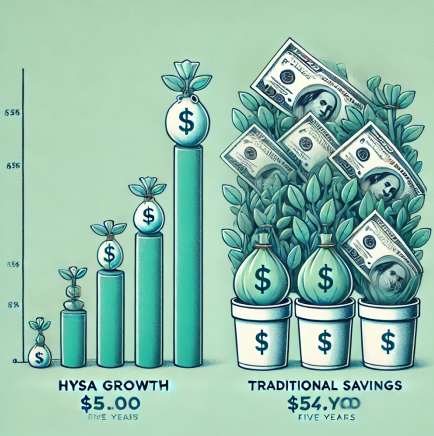

a) Accelerated Compound Interest

Compound interest—earning interest on your interest—supercharges savings over time. For instance, a $20,000 deposit in a HYSA at 5.00% APY grows to $26,532.98 in five years, compared to $20,010.02 in a traditional account.

b) Flexibility for Short- and Medium-Term Goals

HYSAs are ideal for:

- Emergency funds (experts recommend 3–6 months of expenses).

- Down payments for homes or cars.

- Vacation or education funds.

c) Low Risk, High Reward

Unlike stocks or cryptocurrencies, HYSAs guarantee principal protection while delivering competitive returns. This makes them perfect for risk-averse investors or those diversifying their portfolios.

4. How to Choose the Right HYSA for You

Not all HYSAs are created equal. Consider these factors:

a) Interest Rates

Compare APYs across providers. ally and Marcus are on-line banks. Sachs, and Discover frequently lead the market.

b) Fees

Avoid accounts with monthly maintenance fees or excessive withdrawal penalties.

c) User Experience

Look for features like mobile check deposit, 24/7 customer support, and seamless integration with your existing accounts.

5.There are ways to maximise return.

a) Automate Savings

Set up recurring transfers from your checking account to your HYSA. Even $100/month adds up to $1,200 annually, plus interest.

b) Optimize for Taxes

Interest earned in HYSAs is taxable. Consider using tax-advantaged accounts like IRAs for long-term goals and HYSAs for shorter-term needs.

6. The Future of HYSAs: Trends to Watch

AI-Driven Personalization: Banks may soon use AI to tailor savings rates based on customer behavior.

Dynamic Rate Adjustments: Expect more frequent APY changes tied to Federal Reserve policies.

Green Savings Initiatives: Some institutions now offer eco-friendly HYSAs that fund renewable energy projects.

Conclusion

High-yield savings accounts are a cornerstone of modern financial planning, offering a rare blend of safety, liquidity, and growth. There is an emergency fund, No affair what you be building. saving for a milestone, or simply seeking better returns, an HYSA can help you achieve your goals faster. Start by researching top providers, automate your contributions, and watch your savings thrive—one interest payment at a time.

Take Action Today: Audit your current savings strategy. If your money isn’t earning at least 4.00% APY, it’s time to switch.

(Writer:Matti)

Related Articles